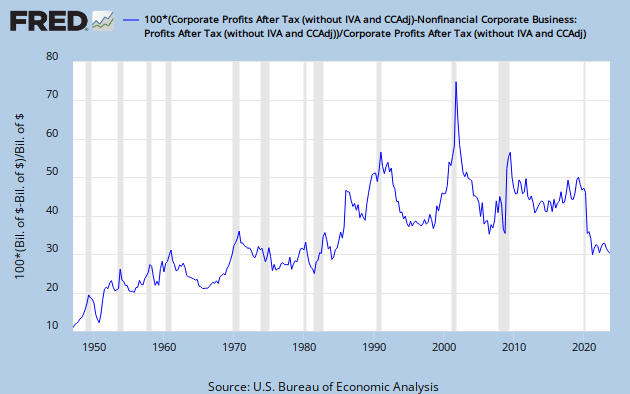

Here is a specific look at the Finance Sector. The graph shows finance sector profits as a percentage of total corporate profits - all after tax.

That's a pretty impressive sweep up over time. I threw some best fit curves through the whole data set, and also though the peaks and valleys. Curves through the extremes are exponential.

Along with the increased percentage we get a dramatic increase in the data spread.

When lines jump around a lot, you can sometimes get clarification by looking at a long average. I tried that here with a 13 year average.

A long average filters out the hash, and reveals the underlying trend. Or, I should say, trends, since there are two, with a sharp break at the beginning of 1986. A best-fit least squares trend line on the data through '85 is a near-perfect match to the average line, which barely even wiggles. We see a bit more action in the post-85 segment, but the new trend is still very clear, indeed. The earlier trend line in green is now the lower channel support line.

The finance sector has captured an increasing fraction of corporate profits, which have been growing at an increasing rate since WWII. And the growth rates are greatest when the economy is doing the worst. Take another look at the first graph. The correlation of finance sector profit peaks with recessions is close to perfect. Peaks are in Q2-1949, Q3-1952, Q4-1953, Q1-1958, Q1-1961, Q4-1970, Q1-1986, Q1-1991, Q4-2001. The peak in 1986 is the only one that does not correspond to a recession.

The finance sector provides a vital function. It is there to facilitate and enable the wheels of industry to turn. But policy matters. What has happened in the age of deregulation and lax taxation is that the finance sector has come to dominate the economy. This is madness. And here is your Great Stagnation, folks.

Beyond the point of supplying necessary financing for businesses and mortgages, financial manoeuvrings - speculation in particular, and most especially so with sophisticated derivatives that nobody knows how to rationally evaluate - become rent seeking. This is a massive misallocation of resources, diverting capital from real investment into totally non-value-added financial tail chasing.

And I'm not the only who thinks so. Here, Paul Krugman calling the whole operation A Giant Scam, quotes Andrew Haldane, Executive Director, Financial Stability, Bank of England:

In fact, high pre-crisis returns to banking had a much more mundane explanation. They reflected simply increased risk-taking across the sector. This was not an outward shift in the portfolio possibility set of finance. Instead, it was a traverse up the high-wire of risk and return. This hire-wire act involved, on the asset side, rapid credit expansion, often through the development of poorly understood financial instruments. On the liability side, this ballooning balance sheet was financed using risky leverage, often at short maturities.

In what sense is increased risk-taking by banks a value-added service for the economy at large? In short, it is not.

Haldane's article was reposted at Naked Capitalism. What he is getting at is the derivatives market, the unregulated darling of the World of High Finance. Estimates vary, since there is no good way to get a handle on it, but the highly leveraged derivatives market has a notional value somewhere between 10 and 25 times the aggregate value of global GDP. In the wake of Phil Graham's undoing of Glass-Steagal came a sea change in the way the Finance Sector does business, and along with this came a shift from risk management to risk-making. As Haldane put it: "If risk-making were a value-adding activity, Russian roulette players would contribute disproportionately to global welfare."

Since none of this activity does anything to create real wealth, it is nothing but rent-seeking. That is bad, in and of itself. Worse, still, in Krugman's words: "Wall Street and the City were con artists extracting huge rents from an unwary public (and eventually dumping much of the cost, when things went bad, on taxpayers)." What is perhaps worst of all is that the money locked up in these ventures is diverted from real investment.

So, here is the picture. While the average earnings of working stiffs has been stagnant, at best, corporate profits have grown at an increasing rate. Further, the percentage of those profits going to the Finance sector has also grown at an increasing rate. Total profit growth is above exponential, and Finance Sector profit growth is super-exponential.

To summarize:

1) Over the last 30 years banking has devolved from a necessary financial function involved in the allocation of resources and management of risk to essentially non-value-added rent-seeking activities implemented through high risk practices.

2) When the whole house of cards came tumbling down, the losses were socialized, while the criminals who perpetrated the underlying fraud walked off not only scot-free, but with huge bonuses.

There might be some way to justify this if it were leading to greater GDP growth or a rising tide that lifted all the boats. But the opposite has happened. GDP growth has been in decline for decades, and the tsunami of profits floating the yachts in the Finance Sector has swamped all the dinghies.

Cross Posted at Angry Bear.

![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_u3HLhk2jOC_E9r_-y_EfhAKi3tcevstQyCBZW5D81vch4lOrFe4_YCqSXm0FSawYkID0V3y9HD-SItjafYdWnteZ6PTwjaAdwbhAWwZ8HJ_b0_HiTU5g3QHGark5K_0D5M=s0-d)

3 comments:

Too many words for my brain, but a really good post.

Glad to discover the FRED series in your first graph.

I line to point out that the economists all speak of financial and non-financial sectors. I prefer to think of those as the financial sector and the productive sector.

Or as the productive and non-productive sectors.

I LIKE to point out... LIKE to.

Ah yes, Art - exactly so.

I try to be thorough, not wordy.

Complex ideas require a lot of explanation. I also wanted this post to be non-refutable.

interestingly, not a peep out of the usual conservative water carriers at the AB cross-post.

Cheers!

JzB

Post a Comment