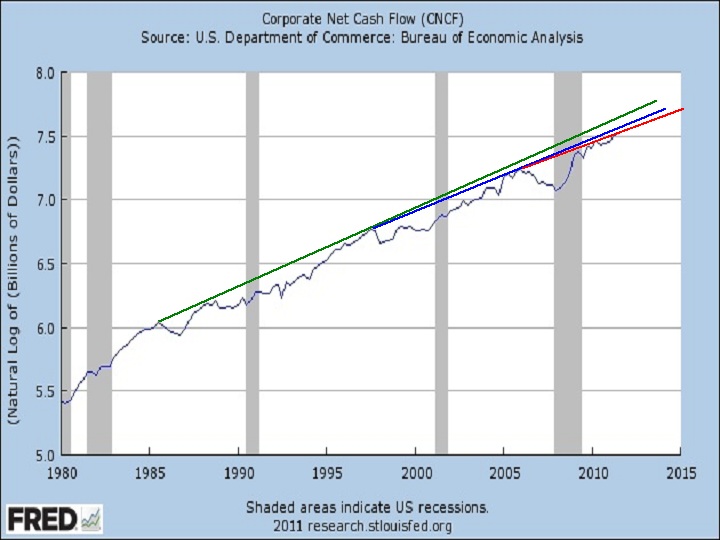

Connecting peak to peak a la Krugman, since 2005, CNCF seems to have established a new trend line (red) at slightly lower slope than the trend line from the late 90's (blue.) This, in turn, has a lower slope than the previous trend line (green) from about 1985.

You'll have to believe me when I tell you a few historical facts (or go to

FRED and look them up yourself.) First, the green line slope is virtually identical to that from 1950 through the early 1970's. Second, the slope from the late 70's through '85 was greater than the green line slope (you can see that in this chart if you look to the left.) Third, the slope through the mid 70's was greater still.

Restated, the growth of CNCF has never been slower in the post WW II period than it is right now. Yet

Karl Smith is excited about current growth, is making optimistic predictions about 2012, and expects inflation.

My comment:

Karl and I can't both have it right. Which of us do you think is wrong, and why?

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/tny_au_xx_usoz_4.gif)

I am one who so objects, and I certainly haven’t missed it.

http://jazzbumpa.blogspot.com/2011/06/labors-share.html

How can increasing corporate profits, per se, be inflationary? This just enables even greater wealth disparity. A falling labor share means most people get squeezed out of buying discretionary items. Hence, a continuing (and increasing?) aggregate demand shortfall,

I’d love to see a detailed explanation of how inflation can increase in this scenario.

BTW – put your graph on a log scale and you’ll see your CNCF/GDP ratio climbing during recessions, and very dramatically during this last one. Such was not usually the case before about

1970 (recession ca. 1955 is the exception.)

http://research.stlouisfed.org/fredgraph.png?g=3yb

Also, beware the denominator. Progressively lower GDP growth since ca. 1980 skews your ratio upward.

http://research.stlouisfed.org/fredgraph.png?g=3yd

JzB