I'm not here to defend the Fed, but there are two issues. The first issue is their behavior - and if they mistook 2008 for 1978, that is inexcusable.

And, as Marcus points out, it looks like they did. [Emphasis his]

Two speeches by voting Regional Fed presidents certainly helped perceptions along:

Plosner (July 22): Keeping policy too accommodative for too long worsens our inflation problem. Inflation is already too high and inconsistent with our goal of — and responsibility to ensure — price stability. We will need to reverse course — the exact timing depends on how the economy evolves, but I anticipate the reversal will need to be started sooner rather than later. And I believe it will likely need to begin before either the labor market or the financial markets have completely turned around.

Hoenig (July 16): “While the comparison to the ´70s can be useful(!), the present economic situation is also different…

However, like the 1970s, monetary policy is currently accommodative(!)…In this environment there is a significant risk that inflation and inflation expectations could move higher in coming months.

Thus, it will be important for the Federal Reserve to monitor inflation developments and inflation expectations closely, and to move to a less accommodative stance in a timely fashion”.

By their words shall you know them. But only if you're paying attention.

Let's look more closely at that first issue - Fed behavior. What was happening with inflation, and how did the Fed react? Graph 1 shows headline inflation in blue and core inflation in red.

In mid 2008, core inflation was running at 2.3 to 2.5%, not far off its decade-long average of 2.2%, and had been pretty stable year to date. Headline inflation, however, had taken a big jump. As Graph 2 shows, headline inflation, now in red, was following the producer price index, in blue, which had taken an even bigger jump.

As these graphs show, core inflation - which is what, if anything, policy makers ought to be reacting to - is much less volatile, and did not look at all like cause for concern. But, as Steve Roth pointed out a while back, fighting inflation is the only part of its alleged dual mandate that the Fed takes seriously. The scorpion has to follow its nature.

Meanwhile, what was the economy doing back in 2008?

As Graph 3 shows, the growth in personal consumption expenditures had been in steady decline from the local high of just over 7% in 2005, was more or less stable through the first half of 2008 at about 4%, but then fell off to 1% in October. It was deeply negative by the end of the year.

Not surprisingly, NGDP growth followed a similar path. See Graph 4

Meanwhile, Real Median Household Income, which had risen modestly from 2005-7, was slumping, probably due to income lost in the housing construction bust. See Graph 5.

So, I think it's right and proper to criticize the Fed for their focus on inflation. With 20/20 hindsight, it looks spectacularly wrong-headed.

The second issue is cause and effect between Fed action and the condition of the economy. Did the Fed really spawn the Great Recession in 2008? David Beckworth says yes, and I believe the Market Monitarist community is unanimous on this point. But let's look at what the Fed actually did. Graph 6 shows the Effective Federal Funds Rate in blue. Also included for reference is the Prime Lending Rate, in red, which follows in lock-step.

The Fed Funds rate was shaved a bit from about 5.25% in the 3rd quarter of 2007, then cut dramatically to 2% by the end of the first quarter of '08. In statements from the Open Market Meetings of August 5 and September 16, the FF target rate was kept at 2%. Clearly, that decision did not hold, as the rate was hovering near 0% by the end of the year.

I hope I'm not misstating the Market Monetarists' stance when I say that they believe the Fed has essentially unlimited power to achieve whatever targets it chooses, and that in managing expectations, Fed words speak louder than actions. In a comment at Beckworth's post, linked above, I asked the following:

Regardless of what the Fed did or didn't say; during the first quarter of 2008, The Fed funds rate was cut in half from 4% to 2%, and between August and December dropped to almost zero.

Why do words [or the absence of words] trump what is actually happening in the real world? What percentage of the population has even the slightest awareness of the FOMC? Why would their announcements influence behaviors in the general population?

On October 8, they announced a 50 basis point cut to 1.5%, then to 1.25% on 10/29, on 12/16 the target was reduced to 0 to 1/4%.

When you consider that until the Fall of '07, the Fed Funds rate was over 5%, they did rather a lot taking it to essentially 0 in about 14 months.

What am I missing?

Part of his answer [read it all here, reposted as a follow-up here] was -

As I noted in the post, the key is to change the expected path of monetary policy. That means more than changing the federal funds rate. It means committing to keeping it low for considerable time like the Fed did in 2003 and signalling it clearly and loudly. With this policy, the Fed would have provided a check against the market pessimism that developed during this time. Instead, the Fed did the opposite: it signaled it was worried about inflation and that the expected policy path could tighten. So, yes, the correct response is far more than just cutting the federal funds rate, it is about setting expectations about the future path of policy and the future economic outlook.

I have a hard time accepting this ignore what I do, pay attention to what I say [or don't say] argument. It has to assume that people are deciding their actions by thinking months or years into the future based on what they think the Fed might do then, instead of reacting to what is happening today. Maybe I'm just disoriented by the time travel, but in a world where the major focus is on the current quarter's returns, I don't think very many actual people behave that way. Nor do I believe that the hoi polloi have even the vaguest awareness of Fed activities, let alone their words.

The Market Monetarist response, from Marcus is, "Interest rates are a terrible (even misleading) indicator of the stance of monetary policy." At his article linked in the first paragraph of this post, Marcus indicates that the true stance of monetary policy is the resulting growth in NGDP - which I believe, as post-hoc as it may be, is the axiom on which Market Monitarism rests.

But there are other reasons to disagree. Krugman provides two. First, "We were in the midst of an epic housing bust, which was in turn causing a collapse in the value of mortgage-backed securities, which in turn was causing a collapse of confidence in financial firms." This strikes me as being a market failure, aided and abetted [if not actually caused] by weak lending standards and lax regulation, and thus totally outside the realm of anything that can be effected by either setting or talking about interest rates, especially after the fact.

Second, "what we actually know is that the panic was in fact fairly short-lived, ending in the spring of 2009. . . . Yet the economy didn’t come roaring back, and in fact still hasn’t. Why? Because the housing bust and the overhang of household debt are huge drags on demand, even if there isn’t a panic in the financial market." Again, it doesn't seem likely that Fed action or words would have any effect on this outcome.

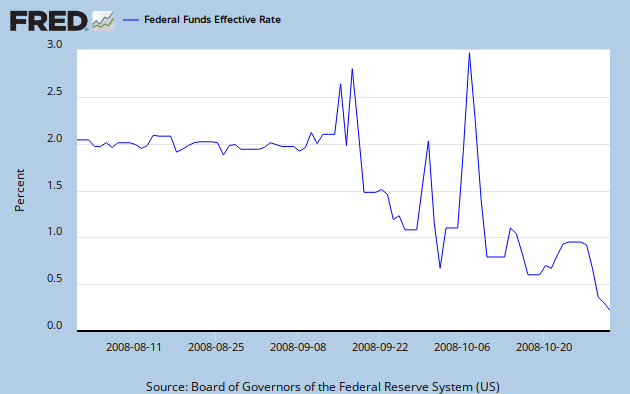

Further, as Stephen Williamson puts it, "So, it's like there was a fire at City Hall, and five years later a reporter for the local rag is complaining that the floor wasn't swept while the fire was in progress." A bit on the snarky side, but he also points out that the Fed had lost control of the Fed Funds rate at this time, anyway, due in part to risk perceptions. This is shown in Graph 7. What does this tell us about expectations at a time of panic?

He also indicated that the Fed loaned substantial amounts to financial institutions, starting early in '08, and increasing dramatically in September and October. This is shown in Graph 8.

Can those words really have been the cause of the greatest financial disaster in 80 years?

Afterthought: It's entirely possible that the Fed, and most particularly bubble denier Alan Greenspan, were complicit in the many-years-long prelude that set the stage for the crash. But that was much earlier and really is a separate set of issues.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/tny_au_xx_usoz_4.gif)

2 comments:

"I have a hard time accepting this ignore what I do, pay attention to what I say [or don't say] argument."

Me, too!

Nice touch, using the graph caption as link text.

Thanks, Art.

JzB

Post a Comment